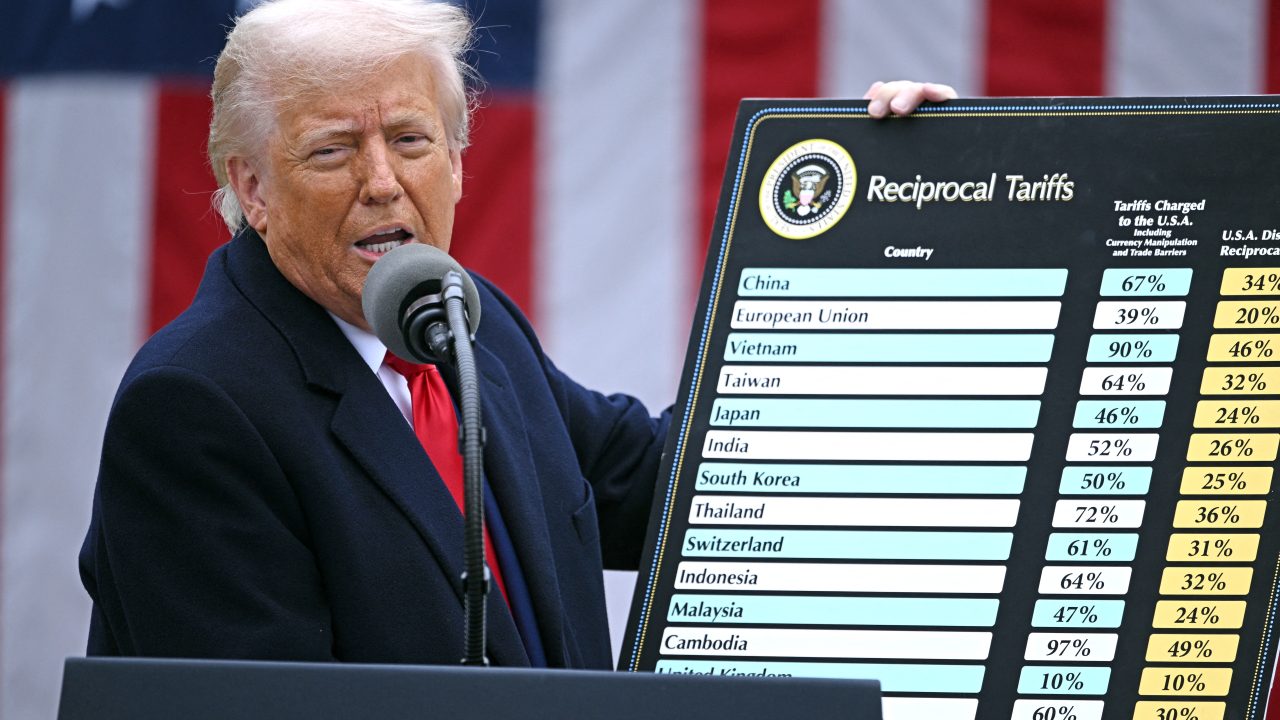

From February 4, when U.S. President Donald Trump imposed 10% tariffs on all imports from China, Beijing and Washington engaged in a three-month back and forth ratcheting up of tariffs. On May 12, after a meeting in Geneva, the two sides issued a joint statement agreeing to lower some tariffs for 90 days while “establish[ing] a mechanism to continue discussions about economic and trade relations.”

That pause offers a chance to consider how China is responding to the changing international trade environment.

The fundamental tension China faces is that the U.S., the world’s largest importer, is explicitly aiming to bring manufacturing back home. That puts China in the crosshairs: It accounts for 29% of the world’s manufacturing output, and, despite increases in domestic consumption and investment, much of that figure turns into exports directed at the U.S.

Aware of the vulnerability that brings — reliance on exports means reliance on potentially unstable external trade relations — China has for a number of years already sought to mediate the risk.

“[B]y the end of 2022 [the Association of Southeast Asian Nations] replaced the European Union as the largest trading partner with China,” Yu Jie (喻潔), senior research fellow on China at Chatham House told their recent panel.

“So I think really Beijing has learned from back to 2018 onward to try to diversify the destination of exports and try to also diversify its source of purchasing agricultural products, which is absolutely essential for the Chinese population, and also try to diversify [the] source of purchasing raw material that would fuel the Chinese economy.”

Yet the intent to shift course does not equate to the ability to do so successfully. The U.S. remains by far China’s largest single-country destination for exports, and significant amounts of the export growth seen elsewhere actually lead back to the U.S.

“A lot of the exports to Southeast Asia are intermediate goods and machinery that are then being used to manufacture products that are being exported ultimately to the U.S. and Europe,” Ben Bland, director of the Asia-Pacific program at Chatham House, said. This could become more of an issue as the U.S. intensifies its scrutiny of exports from Chinese companies operating through third countries — and imposes tariffs on them, too.

“It’s all well and good to talk about the Global South and forming new partnerships with other countries, but how many small developing countries do you have to increase your exports to before you can get to the kind of demand you can tap into in the U.S in one … massive, unified … super wealthy market?” Bland said.

Where do the customers who buy all the stuff China sells come from, if not the U.S.?

Diversification of agricultural and raw material imports present their own challenges, too. Since joining the World Trade Organization in 2001, China’s food self-sufficiency rate — the percentage of food grown internally versus imports — has dropped rapidly, from 94% in 2000 to 66% in 2020. That downward trend is widely expected to continue into 2030. At the same time, Chinese companies extracting raw materials abroad face pressure from third countries to shift toward investing in the refining and processing of minerals within those countries.

Approaching these political and economic headwinds, China’s short-term response has been to push back strongly against the U.S.’s tariffs. On top of imposing its own tariffs on U.S. imports, it announced export controls on critical minerals and initiated a dispute with the U.S. at the WTO.

Coming soon, there may also be attempts to pressure smaller countries away from offering newly favorable trade terms to the U.S.

“Beijing will carefully examine the trade agreement[s] between the United States and the third country and if they have discovered any elements that would actually [harm] China’s interest … Beijing will go after [the] third country,” Yu Jie suggested. This could take the form of making doing business with China “more difficult” or imposing “more stringent” controls over rare earths.

But this does not solve the fundamental problem of where China finds its customers from if the U.S. no longer wants to play that role.

Against that bigger question, David Lubin, Michael Klein senior research fellow at Chatham House’s Global Economy and Finance program, offered two longer-term possibilities for where China goes next.

Option one is that China could erode its trade surplus and “current account balance” by replacing the U.S. as the world’s leading importer. By doing that, it could enrich Global South countries, and enable them to buy its higher-end technology products. But eroding its trade surplus would mean eroding “a kind of insurance against geopolitical risk by keeping the world at a distance from China … limiting China’s dependence on the rest of the world,” Lubin said.

That leaves a second option as more likely, according to Lubin.

“[I]f Trump really can implement this vision of wanting to withdraw from the world, it’s very difficult to imagine big economic powers stepping up to that plate [by becoming alternative large importers.] And so … I think the global macro-consequence of this is a sort of permanent downward shock to global trade growth, a permanent downward shock to global GDP growth.”

In other words, China may not be able to square the circle, but it won’t be alone in feeling the effects.

Leave a Reply